Tambien se dispone en:

![]() Français

Français ![]() Español

Español ![]() Indonesia

Indonesia ![]() Português

Português

Micro-loans, micro-industry, low-tech mushrooms, chickens and goats create employment, income and hope in the developing world. This is a guidance page for project leaders but if you are a visitor looking for capital, funds or loans to start – you are also welcome. You will find a list of funding sources at the end of the page.

For the Goat Bank that gives a future to orphans click here

For a beautiful showcase of different projects click here

Where does Banking for the Poor come from?

During the last 25 years micro-loans for micro-business have been our means of helping a lot of poor people in Africa and India to move towards self-sufficiency and the ability to help others in their family and in their churches.

The inspiration for such a loan granting “Bank” came originally from Deuteronomy 15, 7-11 in the Bible.

“But if there are any poor people in your towns when you arrive in the land the Lord your God is giving to you, do not be hard-hearted or tight-fisted towards them. Instead be generous and lend them whatever they need. Do not be mean spirited and refuse someone a loan because the year of release is at hand. If you refuse to make the loan and the needy person cries out to the Lord , you will considered guilty of sin. Give freely without begrudging it, and the Lord your God will bless you in everything you do.”

How do you do open Banking for the Poor or Community Bank?

1. With a team of interested people you study the issue and then raise start-up capital for your bank, say $500 to begin with, from friends, supporters, investors and partners some of whom might be overseas, but only if that is really necessary. There is a list of agencies that you can approach at the end of this page. Jesus said to some of his servants to whom he had entrusted money, “Put this money to work until I come back.” (Luke 19.13)

2. You announce the availability of micro-loans to one local village or group at a time. You tell the people that credit is available to borrow in small amounts for the one purpose of creating genuine self-employment through micro-industries or working from home with the sole goal of being able to raise the client and his or her the workers to a place of self-sufficiency in life and enabling them eventually to be generous towards others.

Savings

DCI feels that any effective banking scheme must involve regular saving by the clients and by the waiting clients before they get their loan. This means that before a client receives a loan they must be registered with the bank and be on the waiting list, and be saving a small amount each month for their own benefit and to prove their reliability and seriousness. Generally, if they save 10 dollars they can borrow at least 90 dollars, or more at the bank’s discretion.

A typical DCI bank will offer either interest-free or very low interest loans of say, $50, $100 maybe up to $150, but no more. The loan has to be repaid over 6, 12 or 24 months in weekly installments out of earnings beginning immediately.

Compared to the commercial bank rates of 18% and above and the loan shark rates of anything up to 100% or more a 0% or 2% rate is welcomed by all and is no burden. Some bank projects do not charge interest at all but expect that the beneficiary brings a gift at the end to increase the capital fund for the use of others. If a gift of products is brought, then these are sold in the markets or churches and the money added to the general fund. As such the fund is revolving, slowly increasing, always going out and always coming back in for others.

3. You take applications for new micro-businesses from women* or men in your community whom are known. They will need to be people with proven faith, integrity, accountability and competence. In DCI we believe in partnership with clients but without control or ownership.

*See the Important Notes you must read

The Bank is governed by your local committee of men and women appointed for the job.

The Committee receive verbal or written applications from widows, orphans and poor people in general of all ages, the usual condition being that these people would be refused by a normal commercial bank. In DCI we have learned to give preference to women, then to the most destitute of people, people without land and skilled people who are trapped in bonded labour. The committee or their representative trains the applicants to understand and handle their simple responsibilities.

A DCI Bank is normally glad to welcome men and women who cannot read or write and are only able to sign with an X or by the muddy imprint of their thumbs. We have no papers or contracts, we trust the poor. We do not ask for security. Of course the applicant, however poor, has be a person of known background and integrity as well as being a faithful member of a congregation, well known to his or her pastor, priest or other spiritual leader of high repute.

The application has to include the explanation of a simple business plan, enough to show that the project has been diligently considered and is expected to be feasible. The applicant must show that they have the skills to do the job, or if not then they should first apply for a loan or a gift for skill training at a known and acceptable school.

There are 7 things that the applications committee will need to know:

- WHAT is the proposal – exactly?

- WHY will this work? Is there a market for the product or service?

- WHO is to be involved – who are the customers, the workers, the supervisors, the advisors?

- WHERE – will the business be located – exactly?

- WHEN will the project start, and when will it be up and running?

- HOW MUCH will it cost to set up the business?

- HOW will it happen – first step, the second step and so on?

4. The applications committee make enquiries about the applicant.

What happens then?

If the application receives the favour of the committee then the applicant receives the money and begins to work on his her project under the regular weekly supervision and self-help meeting of a group she or he must join ,and under the care of the member of the bank committee who calls to collect the repayments. He is perhaps a businessman who has offered his time and experience for this service as his missions offering.

The following practice is essential.

If you do not do this you will have multiple failure of borrowers:

The applicant must join a small number, say 5 or 6, of other applicants in a support group which shares money-making ideas, encouragement and for finds ways out of difficulty or disaster that a member might face in the future. This group must collectively guarantee the loans of each of its members, so if one member defaults then the other members have an automatic interest in helping their friend. If the member disappears then the group take responsibility to repay the loan, but not in the case of death or long-term illness.

The members of this group should also make time to share their faith, pray for each other and the needs of the families and have someone come and teach God’s ways to them as often as they meet together.

As soon as the installments begin to be paid or the loan is repaid in full, the incoming funds are immediately added to the general fund and go out again as soon as possible into the hands of the next approved applicant. The original beneficiary may apply for a further loan to develop their business.

We greatly encourage a savings aspect to the Banking for the Poor loan schemes, where a client will also save a few coins each week and receive interest on her or his savings. Having savings creates a tremendous ‘feel good’ factor, gives the family a reserve to fall back on in an emergency and gives the Banking Scheme an additional source of capital.

DCI Banks have approved projects such as the provision of seeds or young animals, sewing machines, carts, maybe with a donkey, cows, goats, or the provision of market stalls or street food stalls – micro-businesses that soon produce employment and uncomplicated cash returns. You should avoid agreeing to fund any hi-tech or high maintenance items.

In general, during all the years of operation the “DCI Banks” have enjoyed the full cooperation of the applicants, and our only failures have come through war atrocities or the untimely natural deaths of the applicants. Women have been the most faithful borrowers and we have learned from this.

Overall the “DCI Banks for the Poor” have been a great success and have launched a good number of people on the way to the dignity of self-sufficiency and ability to be generous to others.

The Church or Community Collective Scheme

You could think about a Collective Scheme which buys and sells on behalf of the church or community, staffed by competent, honest volunteers. The church elders or community leaders save the profits ready for emergencies. When something happens to a member then a committee would have to decide if the application was true, and if the applicant is honest, worthy and competent to receive a loan.

Important Notes That You Must Read

Is the micro-finance model for you?

Micro-finance without money from the West is possible.

Consider a Savings and Credit Association instead.

Who do you help and who do you not help?

Saving before borrowing.

Loans to married ladies.

Click to see our Photos from around the world.

Schools of Mission, Banking projects, social action

mission, evangelism, church planting and mor

See the Aduku Village Project in Uganda

For the Goat Bank that gives a future to orphans click here

For a beautiful showcase of different projects click here

The DCI Fund no longer takes applications for providing capital for a Banking For The Poor Scheme as we are not able to verify the application or the integrity of the applicants to the level required of us. Neither are we are able to personally supervise the project as is now required by charity law in the United Kingdom.

Major sources of funding for micro-finance and advice are on the following list and you should approach them directly.

2. Five Talents

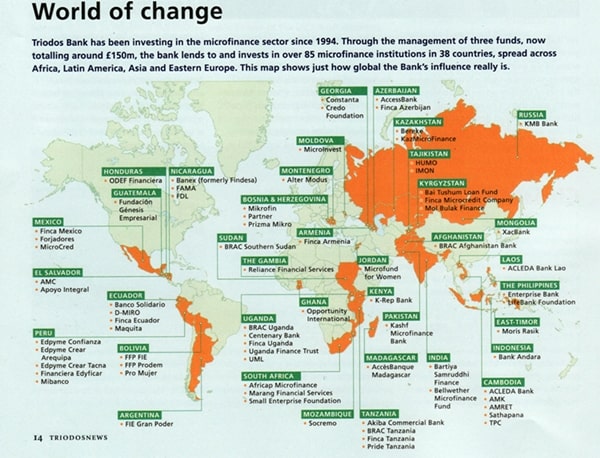

3. Micro-Credit Funds lists many providers of capital for micro-finance worldwide.

3. Micro-credit banks funded by Triodos Bank

4. Shared Interest: Funding for Food Production and Fair Trade